Dividends and Buybacks: How Emart Broke Free From Retail's Valuation Trap [The Answer Is TSR]

As the leading player in South Korea's retail industry, E-mart has not been immune to this stigma of low corporate valuations and depressed share prices.

Recently, however, the company has been shifting the narrative through aggressive shareholder return policies. Observers say Emart is leading a turnaround for retail stocks, breaking free from the shackles of undervaluation.

On April 12, the Korea Financial Times calculated total shareholder return (TSR) using the corporate data platform DeepSearch, covering the period from January 2, 2024 to the last trading day of December 2025. TSR is a metric derived by adding share price fluctuations and dividend yields over a given period and dividing the sum by market capitalization, representing the total return an investor can earn from holding a company's stock.

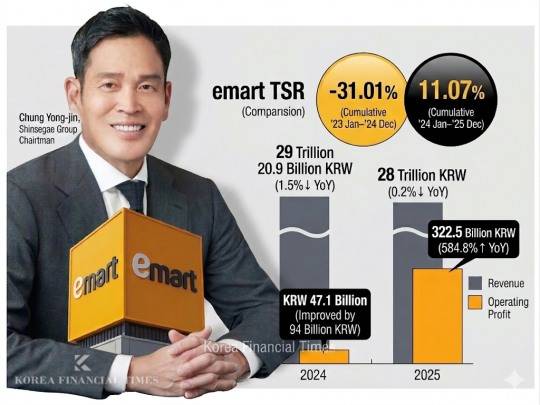

Based on this calculation, Emart's cumulative TSR came in at 11.07%. In practical terms, a KRW 10 million investment in Emart shares at the start of 2024 would now be worth approximately KRW 11.1 million.

By comparison, Lotte Shopping — another major retailer — posted a cumulative TSR of just 2.83% over the same period. With the broader retail sector continuing to trade at undervalued levels, Emart's relatively strong return stands out.

The contrast becomes even more striking when compared with the preceding period.

From January 2, 2023 to the end of December 2024, Emart's TSR was negative 31.01%, meaning a KRW 10 million investment would have shrunk to approximately KRW 6.9 million. The divergence in outcomes depending on the investment timing was stark: those who invested a year earlier suffered losses exceeding KRW 3 million, while those who invested later reaped gains of more than KRW 1 million.

A Dramatic Turnaround in Investment Returns — Why?

Behind Emart's TSR improvement lies an aggressive shareholder return policy. Analysts say the company drove its share price higher by simultaneously expanding dividends and canceling treasury shares to enhance shareholder value.

In the past, Emart's shareholder return policy focused on maintaining stable dividends. Through 2023, the company merely maintained a minimum dividend of KRW 2,000 per share regardless of earnings performance, with limited additional return measures such as treasury share cancellations.

However, as the government's Corporate Value-up initiative gained prominence in 2024, Emart significantly bolstered its shareholder returns.

From 2025 through 2027, the company raised its minimum dividend per share by 25%, from KRW 2,000 to KRW 2,500, and committed to investing an additional KRW 13.4 billion annually to fund the dividend increase.

Treasury share cancellations are also underway. Emart laid out a plan to retire more than 50% of its treasury stock holdings over two years from 2025 to 2026, canceling 280,000 shares per year for a total of 560,000 shares — equivalent to approximately 2% of total outstanding shares. As of last year, Emart's treasury share holdings stood at 2.9% of total shares.

Emart's shareholder return policies were made possible by its stable cash-generating capacity. Despite recording a loss in 2023, the company maintained operating cash flow of KRW 1.13 trillion. It subsequently generated KRW 1.45 trillion in 2024 and KRW 1.32 trillion in 2025, sustaining cash flows above KRW 1 trillion for three consecutive years.

This robust cash generation base is what enabled the aggressive shareholder return policies — including dividend increases and treasury share cancellations — ultimately driving the improvement in TSR, according to analysts.

Core Business Competitiveness Strengthened: Earnings Turnaround Also Plays a Part

The company's efforts to reinforce its core business competitiveness also appear to have played a role.

In 2023, Emart reported an operating loss of KRW 46.9 billion — its first-ever deficit — largely attributable to weakness in its flagship hypermarket operations and deteriorating results at Shinsegae Engineering & Construction.

In 2024, while revenue declined 1.5% year-over-year to KRW 29.0209 trillion, operating profit reached KRW 47.1 billion, an improvement of KRW 94 billion from the previous year.

In 2025, revenue edged down 0.2% to KRW 28 trillion, but operating profit surged 584.8% to KRW 322.5 billion, marking a dramatic improvement in profitability. To improve margins, Emart aggressively pursued operational efficiencies, including organizational streamlining through voluntary retirement programs, integrated procurement across its three offline banners — Emart, Emart Everyday, and Emart24 — and logistics optimization.

While trimming excess, the company doubled down on strengthening its core retail operations.

It opened a series of specialty stores, including Starfield Market locations, Food Market outlets, and warehouse-style discount stores under the Traders brand.

The company sought differentiation through stores tailored to local characteristics and consumer environments. In response to persistently high inflation, it actively invested in value-oriented initiatives, including the budget private-label brand 5K PRICE, the ultra-low-price in-store shop WOW SHOP, and the large-scale promotional campaign Goraeit Festa (a wordplay on the English word "great").

Indeed, Emart's cash used in investing activities reached negative KRW 1.0695 trillion in 2025.

Compared with negative KRW 892.1 billion in 2024 and negative KRW 809.1 billion in 2023, investment spending increased substantially. Industry observers believe that while the strengthening of core business competitiveness and the resulting earnings recovery provided a floor for the stock price, the shareholder return policies served to lift the company's valuation.

An industry insider said, "Emart is a case where an earnings turnaround, core business competitiveness enhancement, and shareholder return policies all converged to push up both the share price and investment returns," adding, "The market's assessment appears to have changed because this was accompanied by fundamental structural improvement, rather than a one-off event."

Park seulgi (seulgi@fntimes.com)

Copyright © 한국금융신문 All Rights Reserved.